NET profits for listed banks in the GCC reached a new record high of $16.2 billion in the second quarter of 2025, marking a 3.7pc increase from the previous quarter and a strong 9.2pc rise year-on-year.

According to an analysis by Kamco Invest, the growth was driven by a broad-based rise in revenues and a lower cost-to-income ratio. This comes despite a sharp 58pc year-on-year drop in project awards, which fell to a 14-quarter low of $28.4bn.

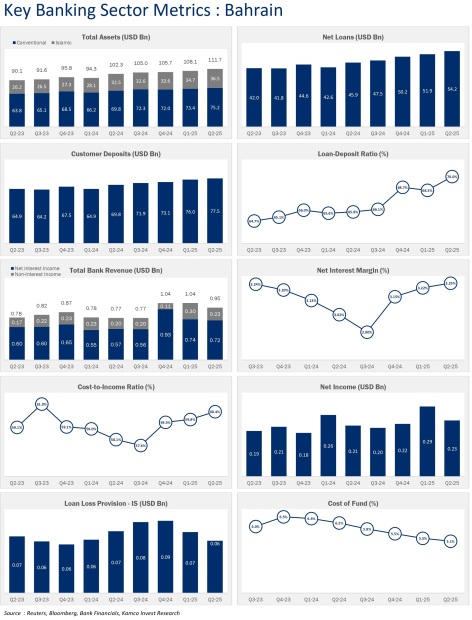

GCC central bank data highlighted the continued resilience of regional economies with strong growth in outstanding credit facilities across all countries except Bahrain.

Five of the six GCC banking sectors saw sequential growth in net income. Kuwaiti banks recorded the biggest profit growth, jumping 15.6pc to add $204.6 million, while the UAE and Saudi banks saw growth of 3.2pc and 2.6pc, respectively.

Aggregate banking sector revenues reached a new peak of $35.6bn for the quarter, a 3.6pc sequential growth. The increase was broad-based, with the exception of an 8.2pc decline in Bahrain’s banking sector revenues. UAE-listed banks led the way with a 5.3pc revenue growth, adding $674m.

Lending growth remained resilient, increasing by 3.4pc to $2.23 trillion — the second-biggest quarterly growth in 16 quarters. The robust performance was a reflection of the strong non-oil sector, with non-oil manufacturing consistently performing well in key regional economies.

Total customer deposits for listed GCC banks also hit a record $2.74trn, a 3.5pc increase. Kuwaiti banks saw the strongest growth in deposits at 4.7pc, followed by the UAE and Saudi Arabia.

The aggregate loan-to-deposit ratio for the GCC banking sector remained high at 81.5pc. Saudi Arabian banks had the highest ratio at 94.3pc.

Aggregate net interest income for GCC-listed banks rose marginally by 0.7pc to $22.9bn, despite rate cuts from the previous year. Net interest margins (NIM) for the sector continued to fall, reaching 3.05pc as a larger share of lending was repriced at lower rates. Bahrain was the only country to see a marginal increase in its NIM.

Impairments booked by GCC banks increased by 12.4pc to $2.4bn, led by increases in the UAE and Qatar. This was partially offset by a net reversal of impairments in Kuwait. The cost of risk for the sector rose slightly to 0.46pc but remains historically low, indicating stable asset quality.

Aggregate operating expenses for the sector declined for the second consecutive quarter, falling 1.5pc to $13.4bn. This resulted in a drop in the cost-to-income ratio to 39.5pc, with Qatari banks boasting the lowest ratio at 36.6pc.

The aggregate return on equity (RoE) remained flat at 13.6pc. The UAE topped the region with the highest RoE at 16.4pc.

avinash@gdnmedia.bh

&uuid=(email))