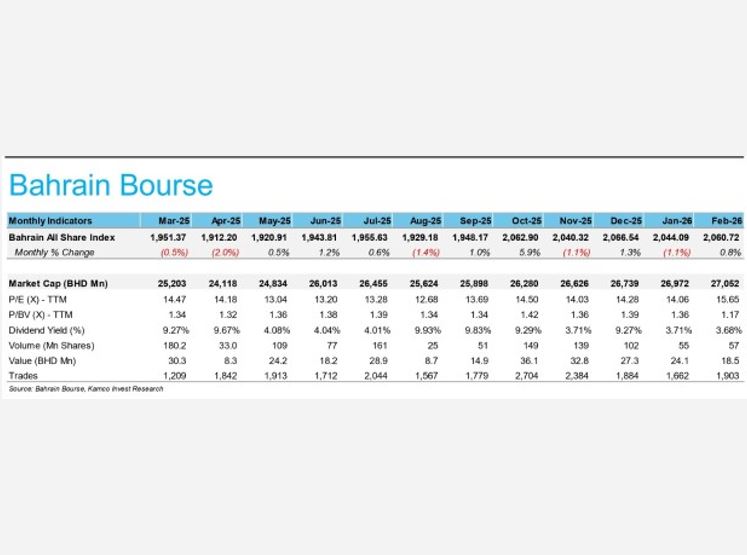

THE Bahrain Bourse (BHB) navigated a month of mixed signals in February 2026, eking out a marginal gain despite a backdrop of challenging macroeconomic news, shows analysis by Kuwait-based Kamco Invest.

The Bahrain All Share Index closed the month at 2,060.72 points, up 0.8 per cent, supported by a predominantly positive trend that saw five out of seven sectors finish in the green.

The consumer staples sector emerged as the month’s top performer, surging 3.5pc to close at 2,534.5 points, closely followed by the real estate sector, which gained 2.2pc. In contrast, the communication services sector bore the brunt of the selling pressure, sliding 1.2pc.

The month was highlighted by the landmark listing of Silah Gulf, a portfolio company of the Bahrain Mumtalakat Holding Company. The Initial Public Offering (IPO), which offered 30pc of the company’s capital at BD0.176 per share, was met with overwhelming appetite. Total demand reached BD11.4 million, resulting in the offer being oversubscribed four times.

According to Bloomberg data, Arab Insurance Group led the individual stock gainers with a 5.6pc jump. BMMI followed with a 5.4pc increase, bolstered by strong fiscal 2025 results. The group reported a net profit of BD7.5m for 2025, a significant climb from the BD6.5m recorded the previous year. Cineco also performed well, rising 4.4pc.

On the losing end, Bahrain National Holding dropped 4.8pc, while Bahrain Islamic Bank (BisB) and Batelco saw declines of 2.4pc and 1.4pc, respectively.

Liquidity on the floor showed a divergence between volume and value. Total traded volume rose 4.3pc to 57 billion shares, with BisB topping the charts at 19.2bn shares.

However, the total value of shares traded plummeted to BD18.5bn, down from BD24.1bn in January. Alba dominated the value charts, accounting for BD7.1bn of the month’s turnover.

Zooming out, GCC equity markets retreated in February as escalating geopolitical tensions between the United States and Iran overshadowed broad gains in global markets, while Oman’s bourse decoupled from its regional peers to post one of the world’s strongest monthly performances.

The MSCI GCC Combined Index fell 2.5pc during the month, pressured primarily by heavy losses in Riyadh and Doha. The decline comes despite a resilient performance in global equities, which advanced even as a “scare trade” related to Artificial Intelligence (AI) valuations sparked volatility in US technology stocks.

Saudi Arabia’s benchmark index dropped 5.9pc, reversing healthy gains from January. Analysts attributed the sell-off to a sharp spike in regional risk premiums following a buildup of US military assets in the Middle East.

Tensions escalated further after Teheran ramped up naval drills and briefly obstructed the Strait of Hormuz, a vital chokepoint for global oil transit, while issuing a Notice to Air Missions (Notam).

“The markets began sliding as soon as the Strait of Hormuz headlines hit terminals,” said one regional strategist. “The geopolitical overlay is currently outweighing local fundamental strengths in the larger markets like Saudi and Qatar.”

Bucking the regional trend, Oman’s stock market surged 16.8pc in February. The Muscat gauge is now up 26pc on a year-to-date basis, making it the region’s top performer.

The rally is being driven by Muscat’s aggressive push for economic reforms as the country seeks inclusion in the MSCI Emerging Market index. Investors have been piling into Omani equities in anticipation of the passive capital inflows that typically accompany an upgrade from frontier to emerging market status.

Elsewhere in the UAE, Dubai and Abu Dhabi benchmarks rose 7.5pc and 4.6pc year-to-date, respectively. Conversely, Kuwait and Bahrain have lagged, with year-to-date declines of 3.8pc and 0.3pc.

Sectoral performance across the Gulf was almost entirely negative in February. The healthcare index recorded the sharpest drop, falling 10.1pc, followed by the food and beverage and consumer durables sectors, which shed 8.4pc and 7pc, respectively.

Large-cap sectors, which typically dictate the direction of the regional indices, saw more measured retreats. The banking sector fell 1.6pc, while the energy index, highly sensitive to the Strait of Hormuz tensions, declined 2.5pc.

Real estate was the sole outlier, gaining 3.6pc during the month, supported by sustained demand in the UAE’s residential and commercial hubs.

avinash@gdnmedia.bh

&uuid=(email))