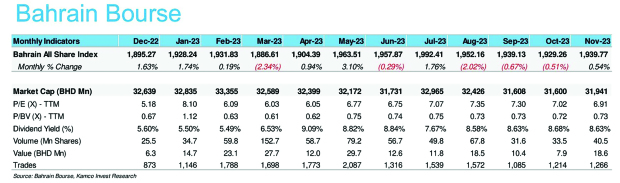

Snapping a three-month losing streak, Bahrain’s equity market closed November 2023 with a gain of 0.5 per cent at 1,939.77 points.

The benchmark All Share Index on Bahrain Bourse (BHB) reported slightly higher returns for year-to-date (YTD-2023) at 2.3pc, according to analysis by Kuwait-based Kamco Invest.

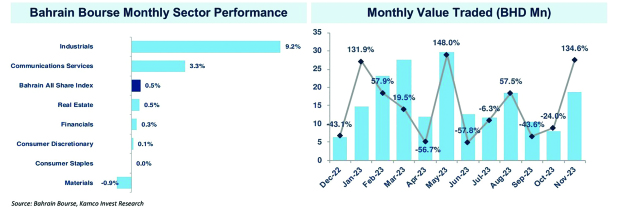

In terms of sectoral performance, the picture was skewed towards gainers after six out of the seven sector indices recorded growth last month.

The industrial sector posted the biggest jump among the sectoral indices at 9.2pc to close November at 2,913.5 points led by APM Terminals Bahrain’s 13.4pc share price surge during the month.

The communications services index and the real estate index followed with increases of 3.3pc and 0.5pc, respectively.

On the other hand, the heavily weighted materials index recorded a marginal decline of 0.9pc to close the month at 4,961.7 points.

In terms of share price performance, according to Bloomberg data, Arab Insurance Group topped the list of gainers with 20.4pc share price rise during the month followed by APM Terminals Bahrain and Al Salam Bank Bahrain with upticks of 13.4pc and 8.2pc, respectively.

On the decliners side, National Hotels Company topped with a 12pc plunge in share price during the month followed by Bahrain Islamic Bank and Bahrain Telecommunications Company with share price drops of 9.3pc and 5pc, respectively.

Trading activity on the exchange picked up during November 2023, with total volume of transactions soaring 21.1pc to 40.5 million shares from 33.5m shares in October 2023.

Similarly, total value traded on BHB soared 134.6pc to BD18.6m last month as compared to BD7.9m during October 2023.

Al Salam Bank Bahrain topped the monthly volumes chart with 19.1m shares changing hands followed by Alba and National Bank of Bahrain at 8.3m and 4.5m shares, respectively.

On the monthly value traded chart, Alba led with BD9m worth of traded shares followed by Al Salam Bank Bahrain and KFH-Bahrain with BD3.7m and BD3.4m in value transacted, respectively.

Zooming out, the GCC regional equity market index advanced for the first time in four months after benchmarks across the region saw a rise during the month.

The MSCI GCC index was up by 5.2pc during November 2023 mainly led by optimism in the global markets following expectations that interest rates have peaked and central banks may start cutting rates next year, most likely during the second half.

The monthly gains lowered the YTD-2023 decline for the region to 2.4pc as four out of the seven regional benchmarks still showed declines while Dubai followed by Saudi Arabia showed healthy YTD returns of 19.7pc and 6.7pc, respectively.

On the sectoral front, almost all regional indices showed an uptick during November 2023, barring the GCC Insurance index that dropped marginally by 0.4pc.

Among the gainers, pharma and biotech led with a surge of 21.4pc followed by consumer durable and apparel and healthcare indices with gains of 14pc and 11.7pc, respectively.

Large-cap sectors like banking showed impressive growth of 6.6pc while energy and materials indices showed relatively smaller advances of 1.8pc and 4.3pc, respectively.

On the international front, almost all key global markets were up during the month with healthy gains.

The optimism pushed the MSCI World index to the highest in almost four months with a rise of 9.2pc, the biggest monthly jump in three years.

avinash@gdnmedia.bh

&uuid=(email))