A GRADUAL de-escalation of regional conflicts and a softening of energy prices remain the baseline for global financial markets, according to the Standard Chartered Global Market Outlook for May 2026.

The report, titled ‘An Uneasy Truce,’ suggests that while a move towards stability is the primary expectation, investors must brace for continued volatility in the absence of a definitive US-Iran diplomatic breakthrough.

In the Gulf region, the investment landscape is characterised by diverging sensitivities to energy and capital flows. Standard Chartered Africa, Middle East, and Europe chief investment officer Manpreet Gill emphasised that market-specific nuances will dictate performance.

“Looking at key markets in the GCC, while Saudi equities tend to be more sensitive to energy prices, this means they potentially have greater resilience in the current environment,” Mr Gill noted.

Conversely, he advised a more cautious approach to the UAE, explaining that UAE equities are more sensitive to foreign flows and the performance of listed sectors like real estate and financials. Consequently, greater selectivity may be required, though the bank has begun searching for value within these sectors.

For fixed-income investors, Mr Gill highlighted an opportunity in high-quality debt, noting that the bank continues to favour the credit quality of investment-grade bonds. This preference is particularly strong within sovereign and sovereign-linked sectors, where any easing of valuations would be viewed as an ideal opportunity to add to existing positions.

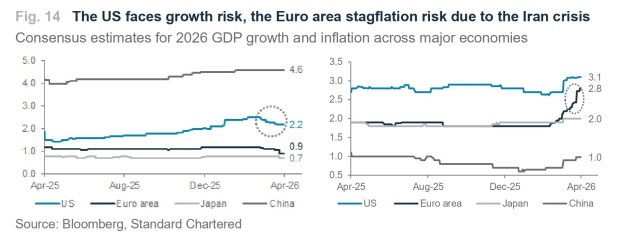

Despite geopolitical headwinds, Standard Chartered remains ‘overweight’ on equities, projecting that robust corporate earnings will outweigh broader macroeconomic concerns.

In the United States, the market is expected to be spearheaded by the technology and communication services sectors, which benefit from a resilient earnings outlook and a lower dependence on Middle East energy compared to other global regions.

The strategy for Asia ex-Japan also remains positive, driven by a weakening US Dollar and robust regional earnings growth. Analysts are currently employing a ‘barbell’ approach to the region, focusing heavily on the AI-driven markets of China and Taiwan on one end, and India on the other, which is expected to benefit from light investor positioning and the downward trend in oil prices.

Safe-haven demand continues to bolster the case for gold, which remains a core recommendation. The bank has set aggressive price targets for the precious metal, forecasting a rise to $5,200/oz over a three-month horizon and reaching $5,500/oz within the next 12 months.

Energy remains the focal point for global stability. Standard Chartered expects WTI crude oil to settle between $80-90/bbl over the next quarter. While the potential reopening of the Strait of Hormuz is a positive signal, analysts warn that physical supply will lag due to upstream and export infrastructure damage, which will delay a return to pre-conflict output levels. A return to the $70/bbl range is considered unlikely before next year.

In the bond markets, the bank is prioritising Emerging Market (EM) debt in both USD and local currencies, citing attractive yields and bolstered fiscal positions in these economies. This stands in contrast to their ‘underweight’ stance on developed market government bonds, which are currently viewed as offering lower relative value.

While the global economy is significantly more energy-efficient than during the shocks of the 1970s, the report concludes that the current environment is far from settled. Standard Chartered advocates for a disciplined, risk-based approach to rebalancing, as any renewed surge in hostilities remains a key risk that could disrupt the fragile stability of the current market.

avinash@gdnmedia.bh

&uuid=(email))