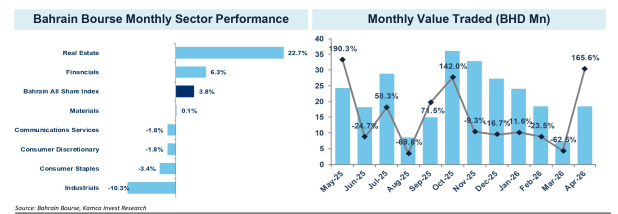

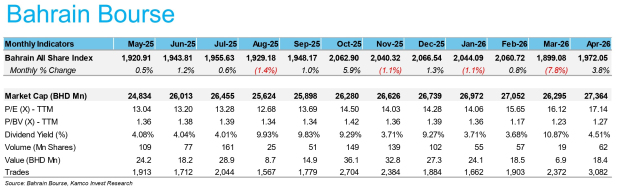

The Bahrain Bourse (BHB) All Share Index staged a strong recovery in April 2026, recording a 3.8 per cent gain to close at 1,972.1 points.

Analysis by Kamco Invest shows that this performance marked the third-highest growth among GCC exchanges for the month.

It helped recoup a portion of the steep 7.8pc decline witnessed in March.

While the overall market trend remained cautious, with four of the seven sectors ending the month in the red, the index found solid support from heavyweights in the real estate and financial sectors.

The real estate sector led the charge, surging 22.7pc to close at 2,779.7 points, while the financial sector followed with a 6.3pc increase and the materials sector saw a modest rise of 0.1pc.

Conversely, the industrial sector faced the month’s sharpest pullback, declining 10.3pc to close at 2,523.4 points.

According to Bloomberg data, Seef Properties was the month’s standout performer, with its share price jumping 38.1pc, followed by GFH Financial Group and Inovest with gains of 27.4pc and 9.7pc, respectively.

On the downside, APM Terminals Bahrain led the decliners with a 12.3pc drop, followed by Gulf Hotels Group (down 6.7pc) and Bahrain Islamic Bank (down 5.1pc).

Market liquidity saw a significant boost in April, with total trading volume soaring by 224pc to 61.7m shares compared to 19m in March.

Total value traded followed a similar trajectory, climbing 165.6pc to BD18.4m from BD6.9m the previous month. Al Salam Bank-Bahrain led the volume chart with 15.6m shares traded, followed by GFH Financial Group (14.2m) and Seef Properties (10.3m).

Regarding value traded, GFH Financial Group topped the list with BD7.9m, followed by Kuwait Finance House-Bahrain at BD4.3m and the National Bank of Bahrain at BD3.9m.

In response to current geopolitical volatility, Bahrain has unveiled a $18.6 billion liquidity support package aimed at stabilising the economy and protecting the private sector.

The measures include provisions for retail lenders and financing companies to grant a three-month deferral on both principal and interest payments for individuals and corporates.

To further enhance liquidity, the Central Bank of Bahrain (CBB) has extended its repo facility to three months, lowered reserve requirements from 5pc to 3.5pc to encourage lending, and reduced the minimum liquidity coverage ratio and net stable funding ratio from 100pc to 80pc.

Additionally, banks have been granted increased flexibility in loan classification, and the government is rolling out a private sector wage support initiative valued at approximately BD100m, designed to cover citizens’ wages up to the insured salary ceiling.

Looking at the global picture, the report notes that equity markets staged a sharp April recovery, erasing first-quarter losses.

The MSCI World Index climbed 10pc, marking its largest monthly gain in over five years. This surge was buoyed by a 14.5pc rise in emerging markets and a 9.5pc increase in advanced markets.

US indices led the momentum, with the S&P 500 rising 10.4pc and the Nasdaq surging 15.3pc. Asian markets outperformed with 13pc gains, driven by Japan’s 16.1pc rally on the back of strong earnings and AI-related stocks. Conversely, European markets posted modest, low-single-digit returns as geopolitical headwinds from the Middle East persisted.

In commodities, crude oil hit a four-year high by month-end as military operations fuelled concerns over supply security.

Returning to the region, GCC equity markets lagged the global rally in April 2026, posting only a marginal 0.4pc gain on the MSCI GCC Index after two consecutive months of decline.

Saudi Arabia’s TASI was the region’s sole outlier, slipping 0.6pc as investors moved to book profits. Despite the monthly dip, Saudi Arabia remains the region’s second-best performer year-to-date with a 6.6pc gain, trailing only Oman, which has surged 42.7pc so far this year.

Elsewhere in the GCC, benchmarks remain in negative territory, posting low-to-mid single-digit declines year-to-date.

Sector performance across the GCC was broadly positive in April. While the healthcare, food and beverage, and retailing indices saw minor losses, the transportation and diversified financials sectors outperformed, each recording gains exceeding 9pc.

avinash@gdnmedia.bh

&uuid=(email))