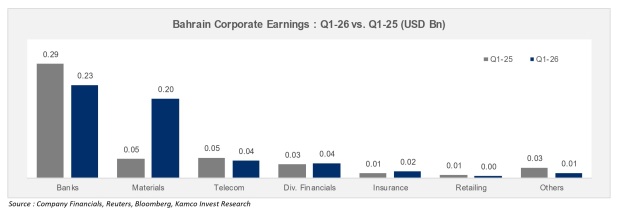

Total net profits for companies listed on the Bahrain Bourse climbed 17.6 per cent year-on-year (y-o-y) during the first quarter of the year, tracking at $549.8 million against $467.6m in Q1-2025.

The latest report from Kamco Invest shows that the gain was carried by strong performance across six of the exchange’s 14 sectors, which managed to offset y-o-y declines in the remaining eight.

Materials, diversified financials, and insurance provided the main lift for corporate earnings during the quarter, whereas the telecom, banking, and retailing sectors weighed on the overall total.

In the materials sector, Alba – the sole company in the category – posted a massive 315.5pc surge in net profit to reach $199.8m for Q1-2026, up from $48.1m in the same period last year.

The bottom-line jump came despite a 17pc drop in sales volume to 312,563 metric tonnes, as regional shipping disruptions took a toll on logistics. Alba managed to overcome the volume drop through stronger average selling prices, which pushed overall revenues up by 2.6pc to BD419.6m ($1.1 billion) compared to BD409m ($1.08bn) a year earlier.

It was a tougher quarter for the banking sector as a whole, with aggregate net profits slipping to $234.9m from $288.5m in Q1-2025. The decline was largely dragged down by a $6.5m loss reported by Khaleeji Bank.

However, the headline sector dip masked strong individual performances from the kingdom’s major commercial lenders. BBK saw its total earnings jump 24.6pc to $70m, a growth trend management credited to its asset and liability strategies alongside expansion in its net loans and advances portfolio. The bank’s net fees and commissions rose 12pc to BD5.6m ($14.9m), helping push total operating income up by 24.6pc to BD50.6m ($134.2m). At the same time, Al Salam Bank booked a 24.4pc improvement in net earnings, which landed at $61.4m for the quarter.

Total net profits for the diversified financial sector rose by 7.5pc y-o-y to reach $37.1m, compared to $34.5m in the opening quarter of last year.

Sector heavyweight GFH Financial Group anchored the growth, reporting a 16.6pc rise in net profits to $35.2m against $30.1m in Q1-2025. The bulk of the momentum came from a sharp increase in wealth and investment management revenues, which brought in $82.5m during the quarter compared to $51.6m previously. Financing and credit operations also saw positive traction, growing 20.3pc to hit $40m.

Zooming out, aggregate net profits for companies listed on GCC exchanges rose 15.5pc y-o-y in the first quarter of 2026 to a record quarterly high of $67.9bn, driven by stronger energy and banking earnings.

Listed companies in the region had posted an aggregate net profit of $58.8bn in the first quarter of 2025, according to financial data.

The quarterly surge was primarily led by profit growth in energy companies, most notably state oil giant Saudi Aramco, alongside gains in listed banks, food and beverage (F&B), and capital goods sectors.

However, sharp profit declines in telecommunications and transportation firms partially offset the overall expansion.

On a sequential basis, profit growth jumped more than 40pc compared to the fourth quarter of 2025, underpinned by higher earnings in the energy, materials, and banking sectors. That quarter-on-quarter growth was slightly dragged down by weaker performance in real estate and F&B.

Regionally, companies listed in Saudi Arabia recorded the largest absolute growth. Net profits for Saudi-listed firms climbed 22.2pc, or $8.1bn to $44.4bn.

Abu Dhabi and Dubai bourses also posted year-on-year net profit increases of $1.5bn and $0.8bn, respectively.

In contrast, companies listed in Qatar and Kuwait saw year-on-year profit declines of 3.3pc and 48.9pc, respectively, though the losses were easily absorbed by gains elsewhere in the GCC.

Sequentially, quarterly profits nearly doubled in Saudi Arabia, offsetting quarter-on-quarter declines in Abu Dhabi, Dubai, and Kuwait. Qatar and Bahrain also tracked double-digit sequential profit growth.

Total quarterly revenues for GCC-listed companies saw a broad-based year-on-year increase of 7.7pc, reaching $353.3bn in the first quarter of 2026.

However, sequential revenue growth slowed to 2.7pc compared to the previous quarter. The slower quarter-on-quarter momentum reflected a widespread revenue cooling across most GCC countries, as regional corporate activity felt the impact of ongoing conflict in the Middle East.

avinash@gdnmedia.bh

Bahrain Corporate Earnings: Q1-2026 vs Q1-2025 (USD Bn)

&uuid=(email))